Deal advisory is the discipline of running a transaction end to end – from origination and target screening through diligence, negotiation, signing and closing. In Vietnam, where approvals and provincial practice shape every timeline, deal advisory is less about financial modelling and more about sequencing. Here is the lifecycle as it actually runs.

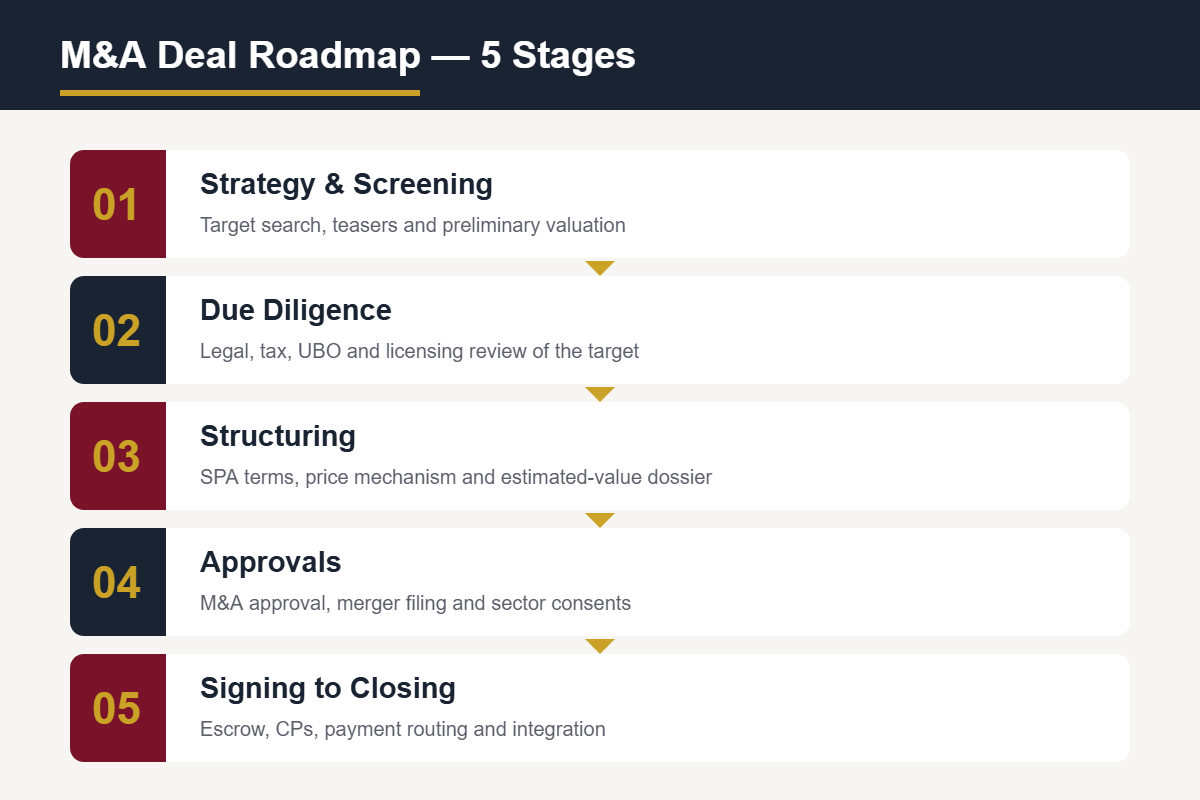

The seven stages of deal advisory in Vietnam

1-2. Origination and screening

Good deal advisory starts before the target list: defining what the buyer can lawfully own, in which sectors, at what ownership percentage. Screening against foreign ownership limits first saves months of pursuing targets the licence regime will not deliver.

3-4. Valuation and structuring

Pricing and structure move together in Vietnam. A share deal preserves licences but inherits history; an asset deal cuts liabilities but reopens permits. The structuring memo should be settled before the letter of intent, because it dictates the approval path and the tax bill.

5. Due diligence

Diligence is where Vietnamese deals are won or repriced. The legal due diligence exercise runs beside financial and tax reviews under one coordinating adviser – the arrangement that stops findings falling between workstreams.

6-7. Documentation and closing

The share purchase agreement converts findings into price adjustments and indemnities; closing then runs through M&A approval, payment through the correct capital account, and registration of the new ownership. Deal advisory earns its fee here, chasing conditions precedent nobody else owns.

What separates strong deal advisory from a broker with a mandate

A broker introduces; deal advisory delivers. The numbers side of the lifecycle is covered in our financial advisory guide; execution detail sits in the transaction advisory workstreams. The difference shows in three places: a written timeline with owners for every approval; negotiation support grounded in what Vietnamese counterparties actually accept rather than imported precedent; and post-signing management – the sixty to ninety days where unmanaged deals quietly die. Ask any candidate adviser to show the closing checklist from their last transaction; the answer tells you everything.

Deal advisory FAQs

How long does a Vietnamese private M&A deal take?

Six to nine months from term sheet to closing for a mid-market deal with foreign-investor approval; faster only when the target file is already clean. Competitive sell-side processes compress diligence but not the statutory approvals.

One adviser or several?

One lead adviser coordinating legal, financial and tax workstreams – with clear scopes for each – closes deals faster than three parallel mandates. On cross-border transactions the coordinating seat belongs with the team that knows the local approval practice; the regulator’s own timelines are published via the Ministry of Finance and provincial portals.

Deal advisory timelines by stage

Origination and screening run four to eight weeks when ownership limits are checked up front. Valuation and structuring overlap across three to five weeks – the structuring memo should close before the letter of intent is signed. Diligence takes three to five weeks for a cooperative mid-market target, longer where land or multiple subsidiaries appear. Documentation runs four to eight weeks of drafting and negotiation, and the approval-to-closing phase adds six to twelve weeks depending on province and sector. Stacked end to end that is six to nine months; disciplined deal advisory overlaps the stages and protects the critical path, which is almost always the regulatory approval.

Budget follows the same curve. The early stages are cheap – screening memos and ownership checks cost days of work and prevent the most expensive category of failure, the deal that could never close. Spend concentrates in diligence and documentation, which is exactly where price adjustments and indemnities are earned. Teams that starve the early stages to save fees routinely pay the difference back at multiple in repriced or abandoned transactions.

The final discipline is the closing checklist: one document, every condition precedent, a named owner and a date for each. On well-run deals it is reviewed weekly from signing; on failed ones it usually never existed.

Sell-side: the same stages, run in reverse

For sellers, the lifecycle starts with vendor preparation – cleaning the corporate file, regularising capital history and licences, and fixing the findings a buyer would otherwise convert into price reductions. A vendor due diligence report, commissioned early, lets the seller control the narrative and keeps competitive tension alive because bidders spend less on their own diligence. Auction discipline then drives value: a two-round process with a locked data room, standardised mark-ups of the sale agreement, and deadlines that are actually enforced. Sellers who prepare for six months routinely recover multiples of that cost at signing, because every defect discovered by the buyer is negotiated at a discount, while every defect fixed beforehand simply disappears from the conversation.

This article is provided for general information only and does not constitute legal advice for any specific case. Regulations may change – please consult a qualified professional before acting. Should further analysis be required, please contact one of our lawyers below.